As housing prices continue to rise, many first-time buyers face substantial challenges in entering the real estate market. To alleviate this burden, some governments are offering financial assistance programs, including a $7,500 grant aimed at making homeownership more accessible. This article explores the details of this government grant, including eligibility requirements, application procedures, and tips for prospective buyers.

What is the $7,500 government grant for first-time home buyers?

The $7,500 government grant for first-time home buyers is a financial aid program designed to assist individuals and families in purchasing their first home. This grant typically does not need to be repaid if the recipient meets specific conditions, making it a valuable resource for those seeking to achieve homeownership.

Understanding the Grant

The $7,500 government grant targets first-time home buyers who may struggle with the financial requirements of purchasing a home. Many state and local governments have implemented these programs to stimulate the housing market and support their residents in achieving economic stability.

Eligibility Criteria

Different states may have varying eligibility requirements for the $7,500 grant. Common conditions include:

- First-Time Home Buyer Status: New buyers who have not owned a home in the last three years usually qualify.

- Income Limits: Many programs set income thresholds based on the area’s median income. For instance, an individual earning over $80,000 in certain metropolitan areas may disqualify for this grant.

- Property Type: The property must often be a primary residence, and condos or single-family homes are typically eligible.

- Credit Score: A minimum credit score requirement may apply, generally around 620 or higher.

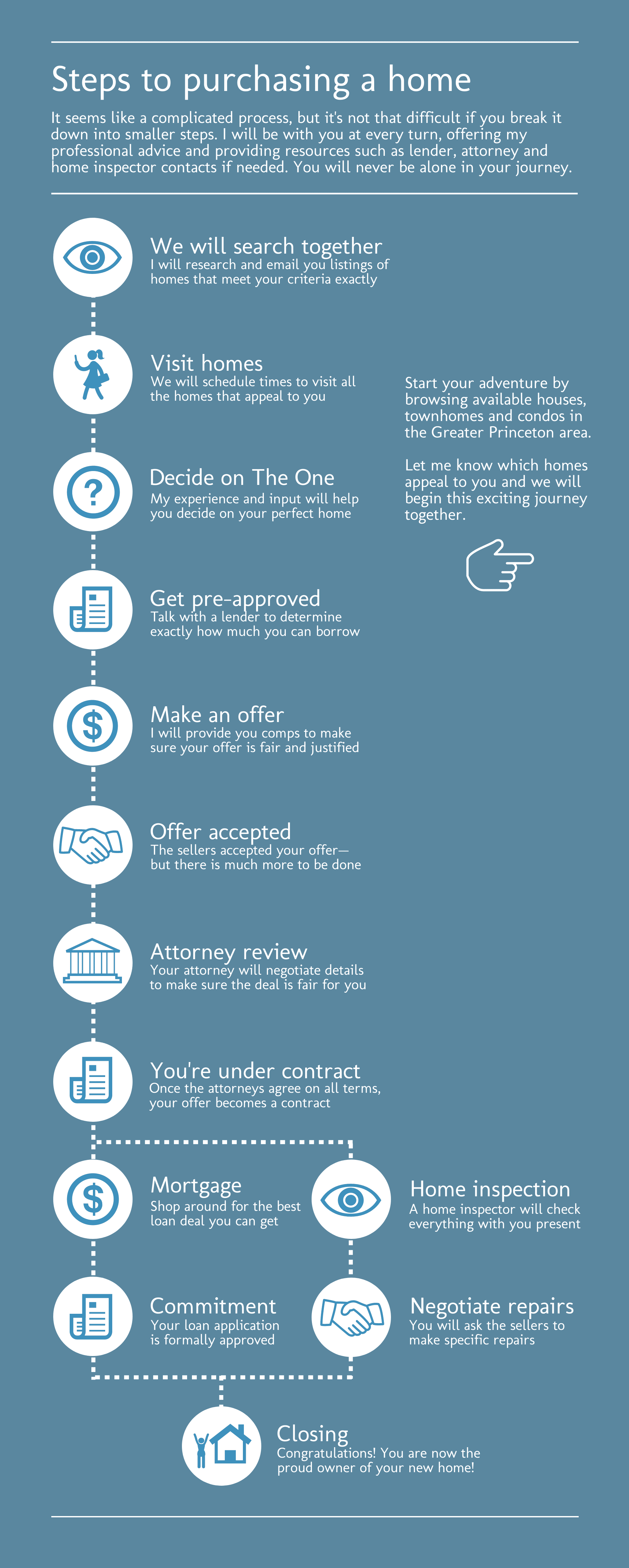

Application Process

Applying for the $7,500 government grant involves several straightforward steps:

-

Research Local Programs: Start by identifying available programs in your state or locality. Websites like the U.S. Department of Housing and Urban Development (HUD) can provide vital information.

-

Gather Documentation: Prepare necessary documents, including proof of income, tax returns, and identification.

-

Complete the Application: Fill out the application form specific to the grant you are applying for. Be meticulous to avoid mistakes that could delay processing.

-

Submit Your Application: Applications can often be submitted online or by mail, depending on the program.

-

Follow Up: After submission, check the status of your application to ensure all steps have been completed satisfactorily.

How to Maximize the $7,500 Grant

To gain the full benefit from the grant, consider the following strategies:

- Combine Resources: Explore additional assistance programs. Many buyers can combine the $7,500 grant with other local or state programs for greater financial aid.

- Budget Wisely: Plan your purchase carefully. Use part of the grant for closing costs or necessary repairs to ensure your home is safe and functional.

Financial Implications of the Grant

Below is a table demonstrating how the $7,500 grant can impact a typical home purchase:

| Expense Category | Average Costs | Grant Contribution | New Cost After Grant |

|---|---|---|---|

| Down Payment (3%) | $15,000 | $7,500 | $7,500 |

| Closing Costs | $5,000 | $2,000 | $3,000 |

| Home Repairs | $2,000 | $1,000 | $1,000 |

| Total | $22,000 | $10,500 | $11,500 |

The table illustrates how the grant can lower the financial burden associated with homeownership, enabling first-time buyers to allocate resources more effectively.

Common Challenges

While the $7,500 grant offers significant benefits, prospective buyers should be aware of challenges they may encounter, such as:

- Limited Availability: Some grants may have a limited number of participants, requiring early application.

- Complex Regulations: Each program may have its own rules, which can lead to confusion and frustration during the application process.

Additional Resources

Prospective home buyers should explore various resources that can offer additional assistance or information, such as:

- Local Housing Authorities: These agencies often provide information about available grants and programs.

- Nonprofits: Organizations dedicated to housing assistance frequently offer free workshops on the home-buying process.

- Financial Advisors: Consulting a financial advisor can help buyers make informed decisions regarding their home purchase.

Conclusion

The $7,500 government grant serves as a significant resource for first-time home buyers, easing the financial burden of purchasing a home. With eligibility criteria tailored to support those in need, this grant can serve as a vital stepping stone for many aspiring homeowners. By understanding the application process, identifying available resources, and planning effectively, individuals can take control of their journey toward homeownership. Whether purchasing a modest starter home or a more substantial property, the knowledge and preparation gained during this process can empower buyers to make informed, confident decisions in their home-buying adventure.

{kind=link}